The average American spends a considerable amount on healthcare each year. Premium increases, higher deductibles and copays, and soaring prescription drug prices can all impact medical costs.

According to the Centers for Medicare & Medicaid Services (CMS), healthcare costs in 2023 skyrocketed to $4.8 trillion1. CMS expects national health expenditures to reach $6.8 trillion by 20302.

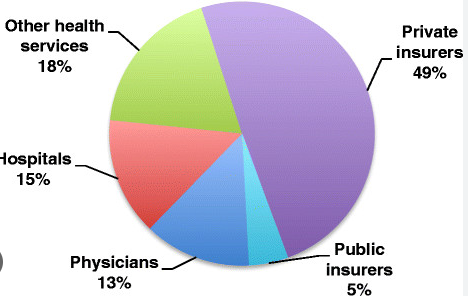

.png?width=647&height=485&name=Screenshot%20(103).png)

With no end in sight to rising healthcare costs, you must understand what causes these spikes. In this article, we’ll look at nine reasons why medical care in the U.S. is so costly. We’ll also show employers how they can help their staff control their medical expenses with a health reimbursement arrangement (HRA).

In this blog post, you’ll learn:

- The top reasons for rising healthcare expenses in the U.S.

- Ways employers can support their employees’ medical needs with HRAs and stipends.

- How personalized health benefits offer potential savings for both employers and employees.

Find out how group health insurance compares to an HRA in our comparison chart.

1. Insurance pays medical providers for quantity, not quality

Most health insurance companies—including Medicare—pay doctors, hospitals, and other providers using a fee-for-service system. This method works by reimbursing each test, procedure, or office visit.

The more services doctors provide, the more money they receive. This can lead to excess testing, overtreatment, or overprescribing. This is particularly true for patients in poor health with a low chance of improvement.

Additionally, the U.S. healthcare system is non-integrated. The World Health Organization defines integrated health services as “the organization and management of health services so that people get the care they need, when they need it, in ways that are user-friendly, achieve the desired results, and provide value for money.”3

So, what does that have to do with cost? Integrated healthcare means providers, management, and support teams work together on a patient’s care. In an unintegrated system, a lack of coordination can lead to duplicate testing and higher costs.

2. The U.S. population is becoming more unhealthy

According to the CDC, six out of ten U.S. adults have at least one chronic disease. Chronic diseases include asthma, heart disease, high blood pressure, or diabetes4. While they may not be rare, illnesses like these can result in higher healthcare costs.

Patients with chronic conditions often need long-term care that’s complex and intensive. This includes more prescription drugs, emergency services, in-home care, and support programs. But these all come with a high price tag.

Roughly 90% of all healthcare costs are for treating chronic illnesses and mental health conditions5. Additionally, 71.6% of adults older than 20 in the U.S. are overweight or obese6. This can lead to chronic diseases and inflated health spending, especially if these patients delay medical care.

As these health issues soar, the risk of insuring the average American increases. The higher the risk, the higher the annual premiums. Over the past decade, the average annual premium for family health insurance coverage rose from $16,351 to $23,968, a rapid increase of 42%7.

3. Newer healthcare technology is more expensive

Medical advances can improve our health and extend our lives. But, upgraded tools can also lead to increased medical spending and overutilization of expensive technology.

Many individuals associate more advanced technology and newer procedures with better healthcare. While this can be the case, there’s one thing for sure—it’s more expensive.

“One of the most influential factors causing costs to rise is technology,” said Raychel Ria, BSN/RN/MPM at MHA Programs. “Healthcare experts are constantly looking for new ways to improve healthcare services. So, medical professionals are researching the capabilities of technology (like AI tools) and implementing many new tech tools. While improving healthcare services is undoubtedly a benefit, the reality is that all of this technology is costly.”

When patients and doctors demand the newest treatments, the costs of healthcare rise for all Americans—even if some don’t support the latest technology.

4. Many Americans don’t choose their own healthcare plan

About 153 million American workers get a health insurance policy through their employers. But, employers typically don’t consult their employees when choosing their group health plan.

Employers often decide their policy based on budget, available health insurers, location, and administrative burden. That means half of Americans don’t make any consumer decisions about the cost of their insurance.

In 2023, the average monthly premium for individuals with employer-sponsored health insurance was:

- $456 for self-only coverage

- $1,437 for family coverage

Each plan will likely have an annual deductible, coinsurance, copayments, and other expenses that can increase out-of-pocket costs.

When private insurers encourage employers to buy expensive group plans for tax reasons, they leave employees in a financial bind. Even low– or no-deductible health plans with small copay amounts can encourage overuse of care. This drives up demand and cost.

5. There’s a lack of information about medical care and its costs

Despite the wealth of information online, there’s no uniform way to understand treatment options and the cost of healthcare. We’d never buy a car without comparing models, features, gas mileage, out-of-pocket cost, and payment options. But this is how we buy healthcare.

According to the Milkin Institute8, only 12% of the U.S. population is health literate. Health literacy is how well people understand basic health information. This lack of knowledge can lead people to make the wrong choices when choosing medical care, which can be costly.

But even when hospitals make their prices available, they’re often challenging to navigate and understand. Congress passed the No Surprises Act in 2022 to mitigate this lack of transparency.

The No Surprises Act aims to do the following:

- Reduce surprise medical bills under private health insurance plans

- Improve the patient experience

- Control costs of health conditions

- Reduce balance billing

- Provide individuals with Good Faith Estimates

6. Hospitals and providers are well-positioned to demand higher prices

Mergers and partnerships between medical providers and insurers are common. These partnerships allow hospitals to expand service offerings, broaden networks, increase access to specialists, and better serve patients.

But, they also reduce individual market competitiveness. The lack of competition allows providers and health insurance companies to drive up their prices unopposed. This can lead to higher hospital charges and lower quality of care.

Consolidated private insurance companies can secure lower prices from healthcare providers because they have more bargaining power. But even so, studies have found that lower provider prices don’t necessarily translate to lower premium prices for consumers.

7. Fear of malpractice lawsuits

Frequently called “defensive medicine,” some doctors will prescribe unnecessary tests or treatment out of fear of facing a lawsuit.

The price for these treatments varies and increases over time. A study found that defensive medicine costs around $46 to $300 billion yearly. This makes up almost 3% of national healthcare spending9. This isn’t surprising, given that our current system supports the fee-for-service model.

About 60% of U.S. surgeons have been sued by a patient during their career10. To avoid this, some surgeons and medical providers perform unnecessary tests to cover all their bases, leading to wasteful health spending.

8. Inflation’s impact on the economy

Healthcare inflation has increased due to patients receiving more medical care. Like other industries, inflation affects medical operations, supplies, administration, and facilities costs. Healthcare facilities have also taken a hit due to staff shortages and lower wages.

As of June 2024, the annual inflation rate was 3%11. But, the medical inflation rate was even higher at 3.3%. Additionally, some medical services and items saw higher prices than others.

| Medical service | Annual inflation rate |

| Hospital services | 6.9% |

| Nursing care facilities | 6% |

| Prescription drugs | 2.4% |

| Medical equipment | 0.8% |

| Physician services | 0.8% |

Many people worry that healthcare inflation will exceed their annual income. So, they cancel or postpone their care until their finances are in order. But, healthcare inflation is often a delayed reaction. Therefore, patients should get healthcare sooner rather than later, especially if they have chronic conditions.

9. The U.S. population is growing older

Baby Boomers make up almost 21% of the U.S. population and are retiring quickly12. According to the U.S. Census Bureau, Americans aged 65 and older will be nearly 23% of the population by 205015. This means the U.S. healthcare system will have more Medicare enrollees.

Because Medicare is a federal government program, more participants impact healthcare costs for everyone. The U.S. spent $944.3 billion on Medicare in 2022.14 CMS projects that Medicare costs will rise by 7.6% annually until 2028 to support future enrollees15.

Older individuals also tend to spend more on healthcare than younger people. They often need frequent primary care services, prescription drugs, or treatment for a chronic condition. Yet, these services and items can lead to wasteful spending and higher medical bills.

How an HRA or stipend can help fight rising healthcare costs

Because healthcare spending continues to rise, it’s a great time to offer your employees a personalized health benefit. One of the best options for small employers is an HRA.

With a stand-alone HRA, you can reimburse your employees, tax-free, for their individual health insurance premiums and out-of-pocket medical costs. HRAs help you manage your health benefits budget and avoid unexpected rate increases. You can also create customized plan designs and give your employees more control over their healthcare spending.

Below are two types of HRAs that are alternatives to a group health insurance policy:

- The qualified small employer HRA (QSEHRA) is for companies with fewer than 50 full-time equivalent employees (FTEs). Organizations can’t offer a group plan with a QSEHRA. With a QSEHRA, employees must have a qualified health plan that provides minimum essential coverage (MEC) to participate.

- The individual coverage HRA (ICHRA) is for organizations of all sizes. Employees must have a qualified individual health plan to participate in the benefit. Those with health insurance through their spouse’s group plan or who take part in a healthcare sharing ministry are ineligible.

If your company already offers a group plan, there’s an HRA for you. Integrated HRAs, or group coverage HRAs (GCHRAs), are for employers of all sizes. With a GCHRA, you can supplement your group plan by reimbursing employees for out-of-pocket medical expenses. Examples of eligible expenses include deductibles, coinsurance, and copays.

Integrated HRAs work with any group health policy. But, you can save even more by using a high deductible health plan (HDHP) with an integrated HRA. You and your employees save money on your monthly premiums, and the HRA will cover out-of-pocket costs that the HDHP may not cover. However, only employees enrolled in your group plan can participate in an integrated HRA.

Employee stipends

You can also offer your employees a health or wellness stipend. With a health stipend, employees receive a fixed, taxable amount of money to spend on out-of-pocket medical bills, including insurance premiums. Employers typically add the extra funds to employees’ paychecks.

You can also offer a wellness stipend to encourage healthy habits, reduce chronic health conditions, and improve morale. These stipends allow you to give your employees money for gym memberships, fitness apps, mental health counseling, and more.

Unlike HRAs, the IRS doesn’t consider stipends as formal health benefits. So, they don’t have as many government regulations. Your employees can spend their money on whatever they choose, even if it isn’t health-related. You also can’t ask them to prove they purchased medical care or require them to provide you with medical receipts.

Conclusion

There’s no one reason to blame for rising health costs. Knowing the key factors can help you understand your options when offering health benefits to your employees. If you’re interested in providing a personalized HRA to offset spikes in healthcare costs, PeopleKeep can help. With an HRA, you can keep your health benefits budget low while providing your employees greater coverage. Schedule a call with an HRA specialist to learn more.

This article was originally published on May 9, 2014. It was last updated on September 3, 2024